All Categories

Featured

Table of Contents

The primary differences in between a term life insurance policy plan and an irreversible insurance policy (such as entire life or global life insurance policy) are the period of the policy, the buildup of a cash worth, and the expense. The ideal selection for you will certainly rely on your needs. Here are some points to take into consideration.

People who possess entire life insurance policy pay more in premiums for less coverage but have the safety and security of recognizing they are protected permanently. 20-year level term life insurance. Individuals that buy term life pay costs for an extended duration, but they obtain nothing in return unless they have the bad luck to die prior to the term runs out

The performance of permanent insurance policy can be consistent and it is tax-advantaged, giving extra advantages when the stock market is unstable. There is no one-size-fits-all response to the term versus permanent insurance policy dispute.

The cyclist ensures the right to convert an in-force term policyor one concerning to expireto a permanent plan without going through underwriting or verifying insurability. The conversion motorcyclist need to enable you to transform to any kind of long-term policy the insurance firm provides without any limitations. The primary features of the motorcyclist are keeping the initial wellness ranking of the term policy upon conversion (also if you later have wellness problems or come to be uninsurable) and deciding when and just how much of the protection to transform.

Who offers Compare Level Term Life Insurance?

Of training course, general costs will certainly increase significantly considering that whole life insurance is a lot more expensive than term life insurance policy - Tax benefits of level term life insurance. Medical problems that create during the term life period can not trigger premiums to be increased.

Whole life insurance policy comes with significantly greater month-to-month costs. It is meant to give coverage for as lengthy as you live.

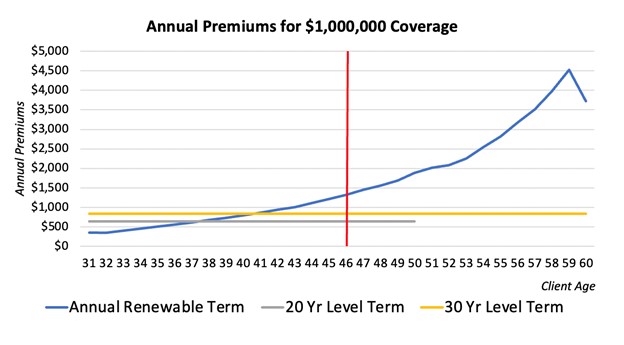

Insurance policy firms established an optimum age limit for term life insurance policy policies. The costs additionally increases with age, so a person aged 60 or 70 will certainly pay considerably more than a person decades younger.

Term life is rather similar to cars and truck insurance. It's statistically not likely that you'll require it, and the premiums are cash down the tubes if you don't. However if the worst occurs, your family members will get the advantages.

What is Level Premium Term Life Insurance?

___ Aon Insurance Solutions is the brand name for the brokerage firm and program administration operations of Affinity Insurance Services, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Fondness Insurance Agency, Inc. (CA 0795465); in Okay, AIS Fondness Insurance Solutions Inc.; in CA, Aon Affinity Insurance Policy Services, Inc.

The Plan Agent of the AICPA Insurance Trust, Aon Insurance Providers, is not associated with Prudential. Team Insurance coverage is issued by The Prudential Insurance Policy Company of America, a Prudential Financial business, Newark, NJ.

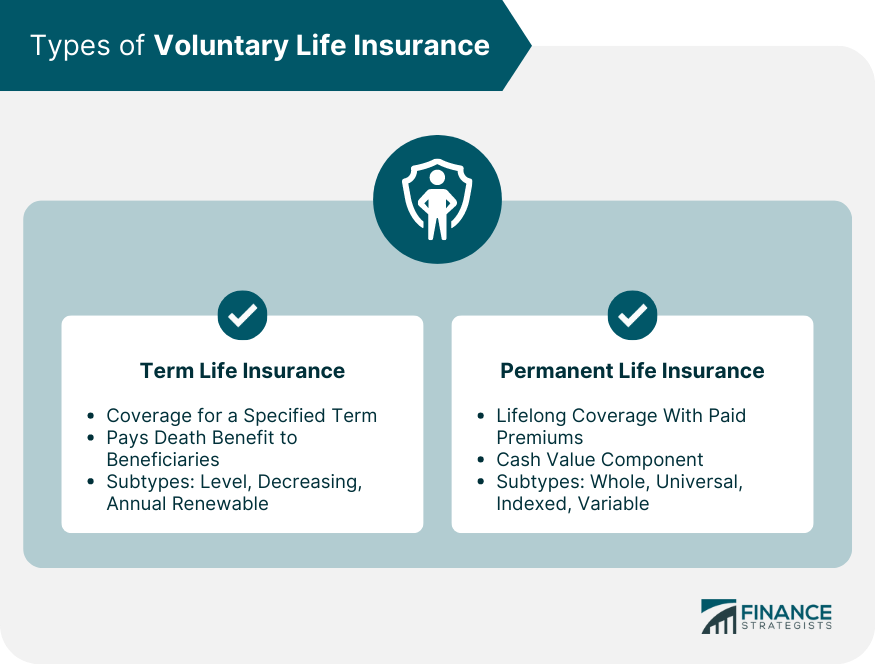

For the a lot of component, there are 2 sorts of life insurance policy plans - either term or permanent plans or some combination of both. Life insurance providers supply numerous forms of term plans and typical life plans in addition to "passion sensitive" items which have actually come to be extra common because the 1980's.

Term insurance supplies protection for a given time period - Term life insurance with fixed premiums. This period might be as brief as one year or provide insurance coverage for a particular number of years such as 5, 10, twenty years or to a specified age such as 80 or sometimes approximately the earliest age in the life insurance coverage mortality tables

Why do I need Level Term Life Insurance?

Currently term insurance prices are really competitive and amongst the most affordable traditionally seasoned. It must be kept in mind that it is a commonly held idea that term insurance is the least expensive pure life insurance policy coverage offered. One requires to assess the policy terms very carefully to decide which term life choices appropriate to meet your certain situations.

With each new term the premium is raised. The right to restore the policy without evidence of insurability is an essential benefit to you. Otherwise, the threat you take is that your health might degrade and you might be not able to obtain a policy at the same prices and even in all, leaving you and your recipients without protection.

The size of the conversion period will differ depending on the kind of term policy purchased. The costs price you pay on conversion is usually based on your "current obtained age", which is your age on the conversion day.

What should I know before getting What Is Level Term Life Insurance??

Under a level term policy the face quantity of the policy continues to be the exact same for the whole duration. With lowering term the face amount minimizes over the period. The premium stays the same each year. Typically such plans are marketed as home loan defense with the amount of insurance decreasing as the equilibrium of the home mortgage decreases.

Typically, insurance companies have not can transform premiums after the plan is offered. Because such policies may continue for numerous years, insurers need to use conventional death, passion and expense rate estimates in the costs computation. Flexible costs insurance coverage, however, enables insurance firms to offer insurance coverage at lower "current" costs based upon less traditional presumptions with the right to transform these costs in the future.

While term insurance is designed to offer defense for a defined period, permanent insurance policy is made to supply insurance coverage for your whole lifetime. To maintain the premium price level, the premium at the younger ages surpasses the actual expense of defense. This added costs constructs a book (cash value) which assists spend for the plan in later years as the price of security increases above the premium.

Can I get Best Value Level Term Life Insurance online?

With level term insurance coverage, the expense of the insurance policy will certainly remain the very same (or potentially reduce if dividends are paid) over the regard to your plan, usually 10 or two decades. Unlike long-term life insurance, which never ends as long as you pay costs, a level term life insurance coverage plan will certainly finish eventually in the future, typically at the end of the duration of your level term.

Due to this, lots of people make use of irreversible insurance as a stable economic preparation device that can serve several requirements. You may be able to transform some, or all, of your term insurance coverage during a collection period, commonly the initial 10 years of your plan, without needing to re-qualify for coverage even if your wellness has altered.

What does a basic Level Term Life Insurance Premiums plan include?

As it does, you might desire to include in your insurance policy protection in the future. When you initially obtain insurance, you might have little financial savings and a huge home loan. Ultimately, your cost savings will grow and your mortgage will reduce. As this takes place, you may wish to at some point minimize your fatality benefit or think about converting your term insurance to an irreversible policy.

So long as you pay your premiums, you can rest simple knowing that your loved ones will certainly receive a survivor benefit if you pass away during the term. Several term plans enable you the capacity to convert to permanent insurance without having to take another wellness test. This can permit you to make use of the fringe benefits of an irreversible policy.

{kind=link}

Latest Posts

Family Burial Insurance

Starting A Funeral Insurance Company

Funeral And Life Cover